Nearshoring Cost: Portugal vs Poland vs Romania vs India

The cheapest hourly rate and the lowest total cost of an engagement are rarely the same number. Here is what the comparison between Portugal, Poland, Romania, and India actually looks like when you account for the variables that matter.

For European companies evaluating nearshore and offshore options, the instinct is to open a spreadsheet, compare hourly rates across countries, and pick the lowest number that still feels credible. That instinct is understandable and almost always wrong — not because cost does not matter, but because the hourly rate comparison omits the variables that determine what an engagement actually costs. Timezone misalignment, communication friction, rework rates, onboarding overhead, and retention risk all compound over the lifetime of a project in ways that never appear in the initial rate card.

This article compares Portugal, Poland, Romania, and India across the dimensions that experienced engineering leaders use when making this decision: direct costs, hidden coordination costs, communication quality, legal and compliance alignment, and long-term retention. The argument is not that Portugal is always the right choice — it is that Portugal wins on total cost of engagement for a specific and important category of work, and that understanding which category matters more than the headline rate comparison.

For companies evaluating dedicated team models or staff augmentation, the framework below is more useful than any rate table.

- Quick Decision Summary

- The Four Destinations: A Structured Comparison

- Understanding the Rate Ranges

- The Hidden Cost Layer: What the Rate Does Not Include

- Portugal vs Poland: The Quality-Cost Trade-off

- Portugal vs Romania: Value vs Lowest Cost

- India: When Offshore Economics Make Sense

- The AI and Advanced Engineering Dimension

- When Each Country Is the Right Choice

- Summary: Which Country for Which Work

- Frequently Asked Questions

Quick Decision Summary

| Your Situation | Where to Look |

|---|---|

| Cost is the primary constraint, work is well-specified | Romania or India |

| Quality-first, European timezone, complex or AI-adjacent work | Portugal |

| Strong technical depth, EU compliance, slightly lower cost than Portugal | Poland or Romania |

| US-based company, timezone alignment with US matters | India or LATAM |

| Building long-term team with high retention and low friction | Portugal |

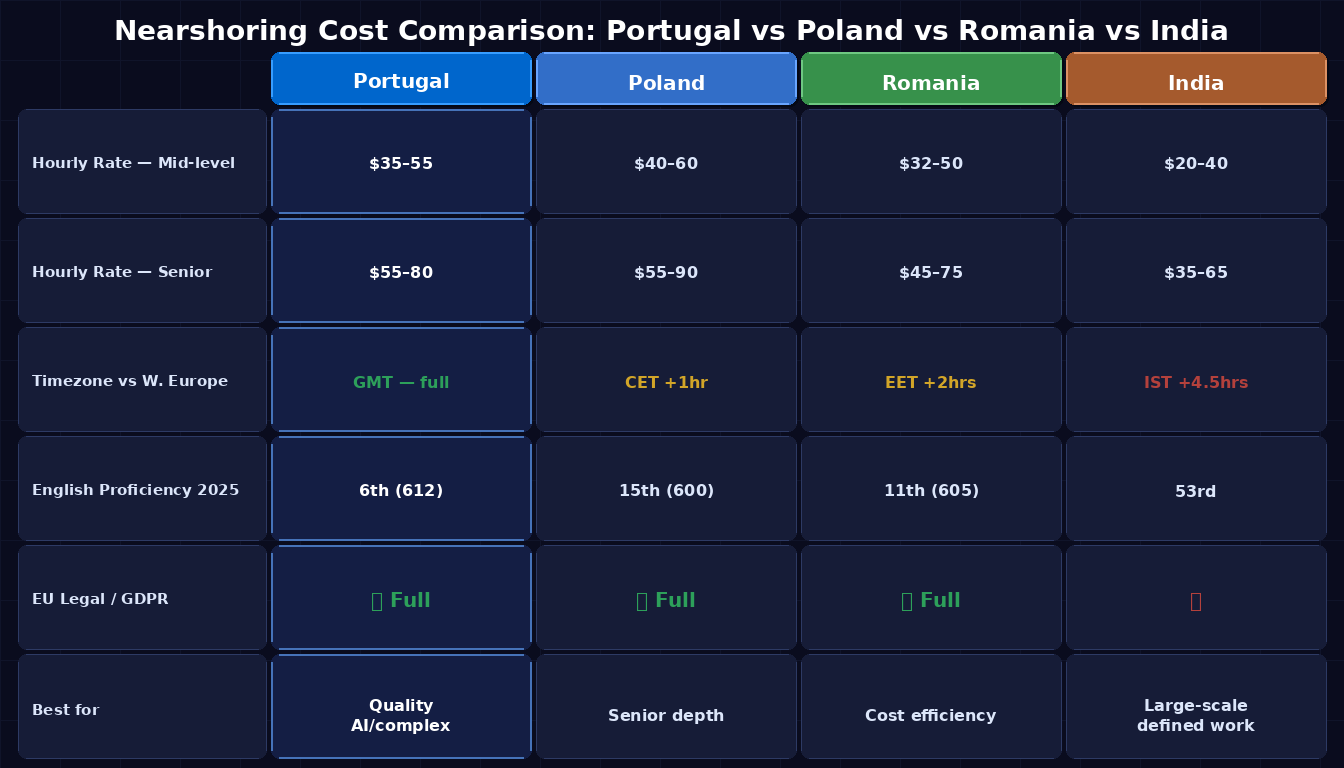

The Four Destinations: A Structured Comparison

| Factor | Portugal | Poland | Romania | India |

|---|---|---|---|---|

| Avg. hourly rate (mid-level, 2025) | $35–55 | $40–60 | $32–50 | $20–40 |

| Avg. hourly rate (senior, 2025) | $55–80 | $55–90 | $45–75 | $35–65 |

| Timezone (vs. Western Europe) | GMT/GMT+1 — full overlap | CET — 1hr ahead | EET — 2hrs ahead | IST — 4.5hrs ahead |

| EF EPI English Proficiency (2025) | 6th globally (612) | 15th (600) | 11th (605) | 53rd |

| EU Legal Framework | ✅ Full GDPR/IP alignment | ✅ Full | ✅ Full | ❌ |

| Talent market saturation | Growing, not yet saturated | Saturated in major hubs | Moderate saturation | High churn at senior level |

| Senior retention signal | High — 48% want to stay* | Moderate | Moderate | Lower at senior level |

| Best for | Quality-first, long-term, AI/complex | Senior depth, EU compliance | Cost efficiency, EU compliance | Large-scale, well-defined, cost-driven |

*Source: Landing.Jobs, Global Tech Talent Trends Report 2025

Understanding the Rate Ranges

The rate data above comes from multiple 2025 market reports including Accelerance's Global Software Outsourcing Rates Guide and DistantJob's 2026 breakdown. A few caveats are worth making explicit before drawing conclusions.

First, the ranges are wide because seniority, tech stack, and engagement model create significant variation within each country. A mid-level React developer in Bucharest costs differently from a senior ML engineer in Warsaw. The figures above represent realistic market benchmarks for mid-level to senior general software engineering talent — not the cheapest available, which tends to be junior-heavy and more expensive than it appears once management overhead is factored in.

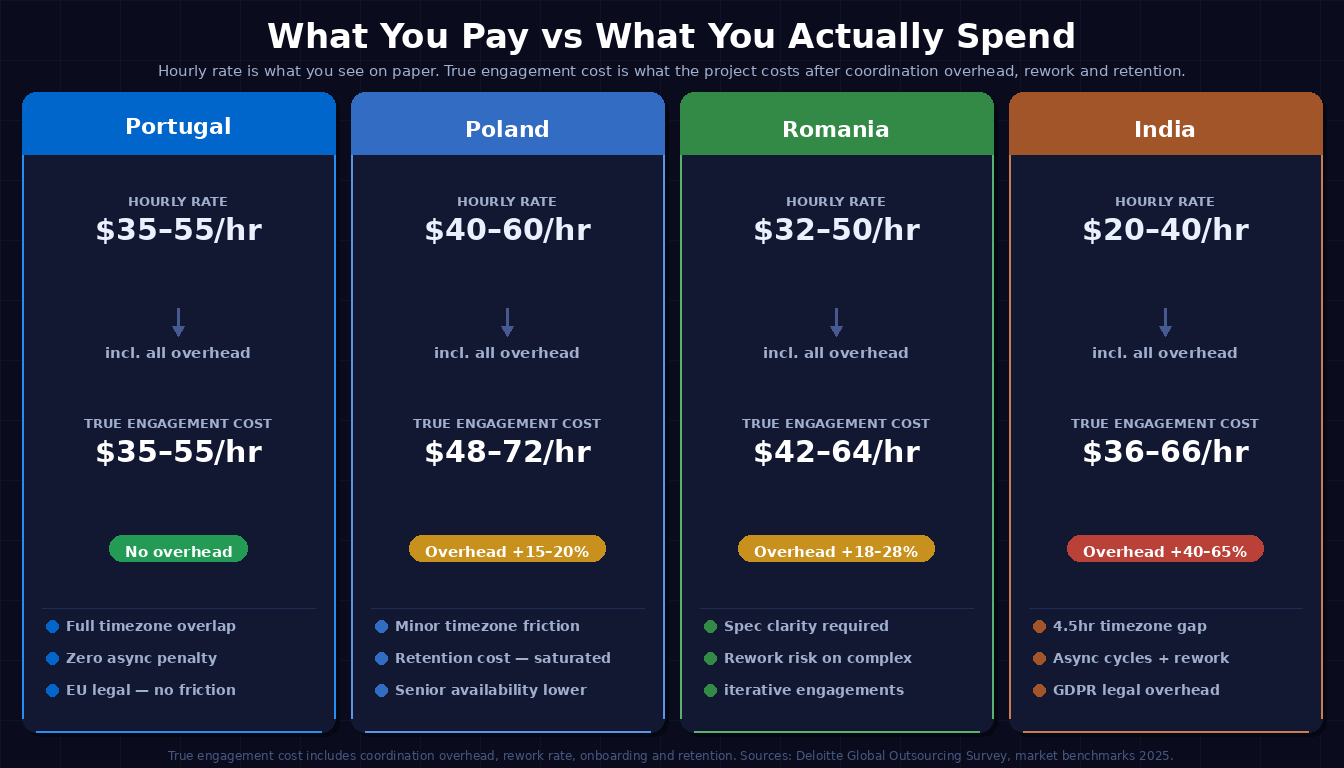

Second, the rates above reflect direct labour cost only. They do not include coordination overhead, which according to Deloitte's Global Outsourcing Survey can account for 15–30 percent of total delivery time in distributed team arrangements. That overhead is not evenly distributed across geographies — it scales with timezone separation and communication friction. This is where the comparison starts to shift materially.

Third, Portugal's rates sit above Romania's and India's on paper. Understanding why the total cost of engagement frequently inverts that relationship requires looking at what the rate difference actually buys — and does not buy.

The Hidden Cost Layer: What the Rate Does Not Include

The variable that most rate comparisons omit is coordination overhead — the time spent managing ambiguity, resolving miscommunication, reviewing work that missed the brief, and re-onboarding after attrition. These costs are real and they compound. A project that runs 15 percent over timeline because of async communication gaps costs more than the hourly rate differential it was designed to offset.

Timezone misalignment with India is the clearest example. With a 4.5-hour gap between India Standard Time and Central European Time, a European company loses most of the working day overlap. A question raised at 9am in Lisbon reaches an engineer in Bangalore at 1:30pm their time. If the question requires a decision or clarification, the answer may not arrive until the following European morning. Compounded over a twelve-month engagement, those delays do not feel dramatic in any individual instance — they feel like normal project friction. But that friction consistently stretches calendar timelines, and research on distributed engineering teams consistently identifies timezone alignment as one of the most underestimated variables in outsourcing decisions.

Poland and Romania largely avoid this problem, sharing European timezone overlap with Western clients. The remaining friction in Eastern Europe tends to come from a different source: market saturation and the senior talent extraction problem. Poland's nearshore market has been absorbing international demand for over two decades. The most experienced profiles in Warsaw and Kraków have often been cherry-picked by German, Dutch, and Scandinavian companies with deep pockets and strong employer brands. What remains is competent but skewed toward mid-level profiles, and senior retention in saturated markets is lower than in markets still scaling up.

Portugal's position in this comparison is structural: it combines European timezone alignment with a talent market that is still in earlier stages of international nearshore absorption. Senior engineers have not yet been systematically extracted by the wave of international demand the way Poland has. That creates a retention dynamic that matters considerably for engagements that last more than twelve months — which most serious software and AI projects do.

Portugal vs Poland: The Quality-Cost Trade-off

At first glance, Portugal and Poland look similar. Both are EU member states with full GDPR alignment, both operate in broadly compatible European timezones, and both have strong technical education systems. The rate differential is real but not dramatic: a mid-level engineer in Lisbon costs roughly the same as one in Warsaw, with senior profiles slightly more accessible in Lisbon at comparable rates.

The distinction that matters more than the rate is the communication quality gap. Portugal ranks 6th globally in the 2025 EF English Proficiency Index with a score of 612, an all-time high. Poland ranks 15th with a score of 600. That gap is not trivial in practice. English proficiency at the level Portugal demonstrates translates directly into the quality of requirements interpretation, the confidence of client-facing communication, and the speed with which a Portuguese engineer will surface a problem rather than work around it. For companies building complex systems — AI pipelines, architectural integrations, platforms with ambiguous specifications — that communication quality is load-bearing.

The pattern that emerges consistently across nearshore engagements in both markets is not that Portuguese engineers are more technically capable than Polish ones — both markets produce genuinely strong engineers. The difference is in integration speed: Portuguese teams tend to reach genuine working velocity faster, with fewer cycles of misaligned output that require correction. That acceleration in the first two to three months of an engagement more than compensates for any marginal rate difference.

Poland remains a strong choice when the work is well-defined, the client has experienced nearshore programme management, and the specific technical depth required — particularly in domains like fintech infrastructure, enterprise Java, or cybersecurity — is the primary hiring criterion. The Polish market's maturity is a double-edged sword: it creates talent saturation pressure but also means deep specialisation in certain verticals that Portugal's ecosystem has not yet developed at equivalent scale.

Portugal vs Romania: Value vs Lowest Cost

Romania is the most cost-competitive EU destination in this comparison. Average hourly rates for Romanian developers sit around $35/hour at mid-level, below both Portugal and Poland, while Romania is a full EU member with complete GDPR compliance and strong technical education — particularly in cybersecurity, fintech, and cloud architecture. For companies with well-defined, volume-driven work and experienced distributed team management, Romania represents genuine value.

The trade-offs are real but specific. Romania's English proficiency ranks 11th globally in the 2025 EF EPI index — strong in absolute terms, but below Portugal. For standardised execution work, that gap rarely surfaces. For complex, iterative work where the specification evolves through dialogue, it creates friction at the margin. Romania's talent market is also experiencing the saturation effects that have been reshaping Poland for longer — rates in Romania have grown significantly in recent years as international demand absorbed the most experienced profiles.

The honest framing is this: Romania and Portugal are not competing for the same engagements. Romania is the right choice when cost efficiency within EU legal boundaries is the primary driver and the work is sufficiently specified to allow asynchronous development cycles. Portugal is the right choice when the work is complex, the integration with the client team is intense, and the cost of miscommunication or rework is high. Companies that try to use Romania for Portugal-type work tend to discover the difference through experience rather than prior analysis — which is the more expensive way to learn it.

What that discovery typically looks like in practice is not a dramatic failure — it is a quiet accumulation of friction. Requirements that were assumed to be clear turn out to need interpretation. Clarification cycles stretch across days rather than hours. Output that technically satisfies the brief misses the intent behind it. None of these are failures of the Romanian team; they are failures of model selection. The work needed a partner close enough to participate in the diagnosis, and it got one optimised for execution. That mismatch is recoverable, but it costs time and often requires bringing in senior oversight that was not budgeted for at the outset.

India: When Offshore Economics Make Sense

India remains the dominant offshore destination globally, and for specific categories of work, the economics are compelling. Companies can save 40–70% compared to Western European rates by engaging Indian development teams. For large-scale, well-specified projects — infrastructure automation, regression testing, data migration, legacy system documentation, defined feature backlogs — India delivers genuine cost efficiency when managed correctly.

The conditions under which that efficiency holds are specific. The specification must be complete before work begins. The interfaces between tasks must be clear. The tolerance for asynchronous communication cycles must be built into the project timeline from the start. When those conditions are met, India's offshore model works as intended. When they are not — when the project is still in discovery, when the requirements evolve through conversation, when architectural decisions need to happen in real time — the timezone gap creates a coordination cost that erodes the rate advantage faster than most projections anticipate.

For European companies, the additional consideration is legal alignment. India sits outside the EU's GDPR framework, which means data processing agreements, IP ownership structures, and contract enforceability require additional legal overhead that EU-based partners do not. For projects handling sensitive data — healthcare, financial services, legal, real estate — that overhead is not minor, and it persists for the duration of the engagement.

The companies for whom India works best in the European context tend to be those with mature distributed engineering practices, experienced offshore programme managers, and work that genuinely decomposes into well-specified, low-ambiguity tasks. That is a specific profile. Companies that approach India as a cost arbitrage solution for complex product development tend to encounter the coordination debt that ultimately pushes the true cost closer to nearshore rates while delivering a slower and more friction-intensive result.

The AI and Advanced Engineering Dimension

The comparison looks different when the work involves AI development, RAG systems, ML pipelines, or advanced integration with existing enterprise infrastructure. These workloads are inherently high in specification ambiguity — the requirements emerge through technical discovery, not through upfront documentation. That characteristic makes timezone and communication quality disproportionately important relative to simpler software development work.

Portugal's position strengthens for this category. The Lisbon and Porto ecosystems have developed genuine AI engineering depth over the last several years, driven partly by the concentration of international technology companies and AI-focused research initiatives in both cities. Portuguese engineers working in AI-adjacent domains are not isolated from global technical standards — they are embedded in an ecosystem that is actively connected to how these problems are being framed internationally. For companies building AI automation workflows, that ecosystem maturity matters.

India has depth in AI engineering that is difficult to match in volume — the sheer number of AI/ML engineers is larger than any European market. But for European companies building AI systems that require close integration with existing enterprise infrastructure, the timezone barrier and the specification clarity requirement become the binding constraint. A RAG system that integrates with a client's proprietary data infrastructure, their existing CRM, and their internal workflows cannot be built asynchronously with a 4.5-hour lag and expect to converge on the right architecture without significant rework cycles.

Poland and Romania both have growing AI engineering communities, and for well-specified AI work — model fine-tuning on clean datasets, infrastructure automation, defined ML pipelines — they represent strong options at competitive rates. The distinction from Portugal re-emerges for complex, integration-heavy AI work where the diagnosis phase and the build phase overlap significantly.

When Each Country Is the Right Choice

The decision between these four destinations follows a consistent logic once you move past the rate table. Portugal is the strongest fit when the engagement is complex and iterative, the specification evolves through dialogue rather than prior documentation, and the client needs genuine same-timezone working overlap with Western Europe. Add to that the EU legal framework — full GDPR compliance and IP ownership without contractual friction — and English proficiency at rank 6 globally, and Portugal becomes the default choice for long-term team building where institutional knowledge and communication quality are load-bearing variables.

Poland serves a different profile: clients who need deep specialisation in specific technical verticals — enterprise Java, cybersecurity, complex fintech infrastructure — where Poland's mature nearshore market has developed genuine depth over two decades of international demand. Poland also works well for well-defined work with experienced nearshore programme managers who understand how to retain talent in a saturated market and are willing to invest in doing so deliberately.

Romania occupies the position where EU legal compliance is required but cost efficiency within that constraint is the primary driver. The work needs to be sufficiently specified to tolerate more structured, less iterative collaboration — but when those conditions hold, Romania delivers genuine value. The saturation dynamic that has reshaped Poland is present in Romania but earlier in its cycle, which means the window of strong value-to-cost ratio remains open, particularly for volume-driven execution work.

India is the right choice when the work genuinely decomposes into well-specified, low-ambiguity tasks, when the scale required exceeds what European markets can provide at short notice, and when the client has mature offshore programme management practices in place. The timezone barrier is real and its cost compounds over a complex engagement — which is why India should not be the default choice for iterative or integration-heavy work for European companies regardless of the apparent rate advantage.

Summary: Which Country for Which Work

Portugal is the right choice when the engagement is complex or AI-adjacent, when full European timezone overlap is non-negotiable, when communication quality is load-bearing, and when you are building a team that will accumulate institutional knowledge over multiple years. The EU legal simplicity and EF EPI rank 6 English proficiency are structural advantages that compound over time.

Poland serves best when specific technical depth in mature verticals is the priority — fintech, cybersecurity, enterprise systems — and when EU compliance is required alongside that depth. The saturation dynamic is real, but it is manageable with deliberate retention investment and experienced nearshore programme management.

Romania is the right fit when EU compliance is required alongside maximum cost efficiency, the work is well-defined and volume-driven, and the client has the programme management bandwidth to work in a more structured, specification-first collaboration model. Romania's value window remains open — but it is narrowing as international demand continues to absorb senior profiles.

India is the appropriate choice when scale exceeds European market capacity, the work is highly specified with clear interfaces and low ambiguity, cost is the dominant constraint, and the client has mature offshore programme management already in place. The timezone barrier is not a dealbreaker for the right category of work — it is only a dealbreaker when the work requires the kind of real-time dialogue that India's model structurally cannot support.

Frequently Asked Questions

Is Portugal more expensive than Poland and Romania?

On headline hourly rates, Portugal is comparable to Poland and slightly above Romania. On total cost of engagement — factoring in coordination overhead, onboarding speed, and retention — Portugal frequently compares favourably, particularly for complex and long-term engagements. The rate difference between Portugal and Romania is real but tends to narrow considerably when full engagement costs are measured.

Why does India appear so much cheaper but get used less by European companies for complex work?

The 4.5-hour timezone gap between India and Western Europe creates an async communication cycle that becomes a persistent drag on complex projects. Every ambiguity, every architectural decision, every requirement change requires a day-long email round-trip at minimum. For well-specified, low-ambiguity work that decomposes cleanly into independent tasks, India works well. For complex, iterative work where the specification evolves through dialogue, the timezone cost tends to erode the rate advantage in calendar time if not in direct cost.

Has Portugal's nearshore market become saturated the way Poland has?

Not yet. Portugal's nearshore scale-up is earlier in its cycle than Poland's, which means senior talent has not yet been systematically absorbed by international demand at the same rate. That creates better availability of experienced profiles and a retention environment that favours multi-year engagements. That window will not remain open indefinitely — the companies engaging seriously with Portugal now are the ones who will have accumulated the institutional relationships and team knowledge that later entrants will find more difficult to build.

Does GDPR compliance really matter for outsourcing decisions?

More than most initial assessments suggest. Companies building systems that handle European user data — healthcare, financial services, legal, e-commerce, real estate — have meaningful compliance obligations that determine where data can be processed and stored, who can access it, and how IP ownership is structured. EU-based partners — Portugal, Poland, Romania — satisfy these requirements without additional legal overhead. India requires specific data processing agreements, IP escrow arrangements, and jurisdiction specification that add both cost and contractual complexity, particularly relevant for regulated industries.

What about English proficiency — does it really matter beyond a basic threshold?

Yes, and it matters more than most evaluations acknowledge. English proficiency below a certain level does not prevent communication — it changes the quality of communication in specific conditions: when requirements are ambiguous, when engineers need to surface problems proactively, when they are engaging directly with client stakeholders. The difference between rank 6 (Portugal) and rank 53 (India) on the EF EPI is not the difference between speaking and not speaking English — it is the difference between fluent professional communication and adequate communication, and that difference is most visible precisely when the stakes are highest.

Can we use a hybrid model — Romania or India for execution, Portugal for architecture and leadership?

Yes, and for the right engagement structure, this can be highly effective. A Portuguese technical lead who owns architecture, client communication, and specification quality, combined with a Romanian or Indian execution team handling well-defined implementation tasks, balances cost and quality appropriately. The model requires investment in the programme management layer and in ensuring the specification handed to the execution team is genuinely complete. When those conditions hold, the hybrid model is one of the more cost-efficient structures available.

How does developer churn affect the cost comparison?

Significantly. Research consistently shows the cost of replacing a technical employee runs between 1.5 and 2 times their annual salary — a figure that includes recruitment, onboarding, and the institutional knowledge that leaves with the departing engineer. Markets with high senior churn impose that replacement cost more frequently. Portugal's retention signal — with 48 percent of tech professionals not wanting to leave the country (Landing.Jobs, Global Tech Talent Trends Report 2025) — directly reduces this hidden cost over multi-year engagements.

If you are evaluating nearshore and offshore options for a specific engineering or AI engagement and want an honest assessment of which model fits your work rather than a rate card comparison, speak with our team. We work across Portugal and European nearshore markets and can tell you what the true cost comparison looks like for the work you are actually trying to do.